1031 Exchange

A Tax Strategy to Unlock Your Real Estate Profits

Get in touch

Thinking of selling your commercial property but worried about capital gains taxes?

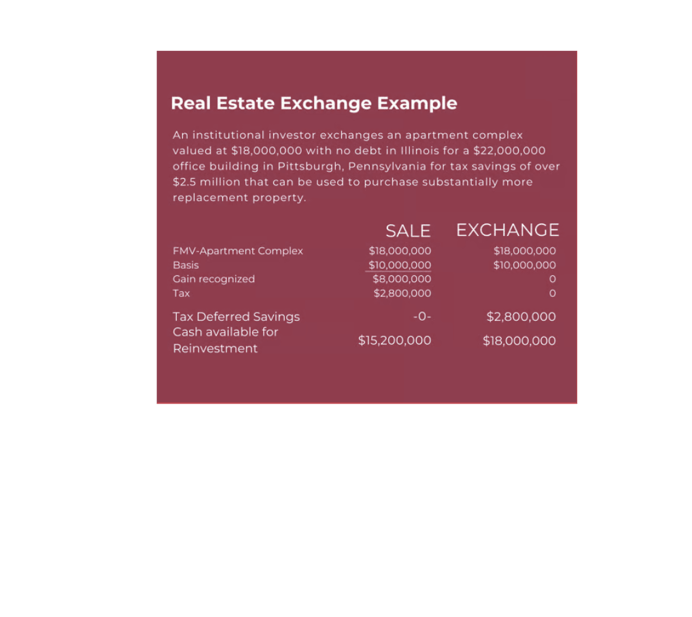

When you sell a business or investment property and make a profit, you usually have to pay capital gains taxes. But there’s a smart strategy called the “1031 Exchange” that allows you to sell your real estate property, reinvest the proceeds in another property of similar or like-kind, and defer paying taxes on that sale. The key here is that the new property must be similar in nature or character, regardless of differences in grade, type, or quality.

For investors, the 1031 Exchange offers several benefits:

Tax Deferral: By using this strategy, we can postpone paying capital gains taxes, which is a significant advantage for our financial planning.

Diversification: It gives us the opportunity to diversify our real estate portfolio by exchanging into different properties.

Tax-Advantaged Cash Flow: Reinvesting in like-kind properties allows us to maintain a tax-advantaged cash flow.

Wealth Preservation: By deferring taxes, we preserve more of our wealth and continue growing it over time .

1031 Exchange Deadlines & Rules

Identification Period (45 Days):

Within 45 calendar days after selling the first property (known as the “Relinquished Property”), the Exchanger must formally identify potential replacement properties.

The identification must be in writing, include the property address or a clear description, and be submitted to the Qualified Intermediary (QI) or another party involved in the transaction.

During these 45 days, you can modify, remove, or add properties to your list as needed.

After day 45, no further changes are allowed.

Failing to identify any properties within this period means you’ll owe capital gains tax on the property you sold.

Exchange Period (180 Days):

The Exchanger must receive the Replacement Property within the earlier of:

180 calendar days from the sale of the Relinquished Property.

The due date (including extensions) for the Exchanger’s tax return for the tax year in which the transfer of the first Relinquished Property occurred.

These timeframes are strict and cannot be extended, even if the 45th or 180th day falls on a weekend or holiday.

However, in certain cases (such as disaster-related issues), an extension of up to 120 days may be possible under Rev. Proc. 2007-56.

1031 Exchange Rules for Identifying Replacement Properties

Three Property Rule:

The Exchanger can identify up to three potential Replacement Properties, regardless of their value.

No need to worry about fair market value; just pick three properties you’re interested in.

200% Rule:

Here, the Exchanger can identify any number of properties.

However, the total fair market value of all identified properties cannot exceed 200% of the value of the Relinquished Properties.

So, you have flexibility, but within a reasonable limit.

95% Exception:

If you identify more properties than allowed by the Three Property or 200% Rules, there’s a catch.

You’ll be treated as if you didn’t identify any Replacement Property unless you actually receive one by the end of the Exchange Period.

This Replacement Property must be worth at least 95% of the total fair market value of all the properties you initially identified.

The value is determined either when you receive the property or on the last day of the Exchange Period.

Contacts

hwest@lee-associates.com

D (412) 284-1650

C (412) 528-1301

O (412) 339-2424

Howard West, Principal

Pittsburgh, Pennsylvania